Planning for future care needs is a topic many individuals and families eventually consider. Long-term care services can provide assistance when someone needs help with daily activities due to age, illness, injury, or ongoing health conditions. Understanding the different types of long-term care services can help individuals become more familiar with the options that may be available. Each type of care is designed to support people with varying levels of assistance, depending on their situation. Below is an overview of several common long-term care service settings.

There’s something special about March in Florida. The weather is just right. The mornings are bright. Outdoor patios are full. Farmers markets are buzzing. It’s the perfect time of year to reset, recharge, and focus on small habits that support long-term well-being. Living well doesn’t require dramatic changes. Often, it’s the simple, consistent actions that make the biggest difference. Here are a few easy ways to embrace healthier habits this spring — right here in the Sunshine State.

Staying informed is one of the most important parts of navigating Medicare and planning for the years ahead. With so much information available online, it can be hard to know which sources are reliable, easy to understand, and actually helpful. To make things simpler, here are three trusted blogs that offer valuable insights on health, wellness, and topics that often connect directly to Medicare decisions. These resources are a great starting point for Florida residents who want to stay educated and confident as they review their options.

The Medicare Open Enrollment Period (OEP) happens every year from January 1 through March 31, and it gives Medicare Advantage (Part C) members a valuable opportunity to make changes to their coverage. But many people confuse OEP with the fall Annual Enrollment Period (AEP), which follows different rules. To help you make confident decisions, here’s a clear and simple breakdown of what you can and cannot do during Medicare’s OEP—so you understand your options and avoid costly mistakes. As a licensed, independent insurance agent, I’m here to guide you through these rules and help you evaluate your needs.

Traditionally, retirement meant a complete shift away from employment. Today, many individuals are choosing a more gradual approach. Partial—or phased—retirement allows you to reduce work hours, modify your role, or transition to part-time or consulting work while continuing to earn income. This approach can help ease the financial and lifestyle changes that accompany full retirement.

Choosing Medicare can be confusing—especially when it comes to picking doctors or specialists. The big question many ask: Can I really see any provider with my Medicare plan? In short, it depends on which type of Medicare coverage you have. This guide breaks down your options, explains how provider networks affect your access, and shows you exactly how to check if your provider is covered.

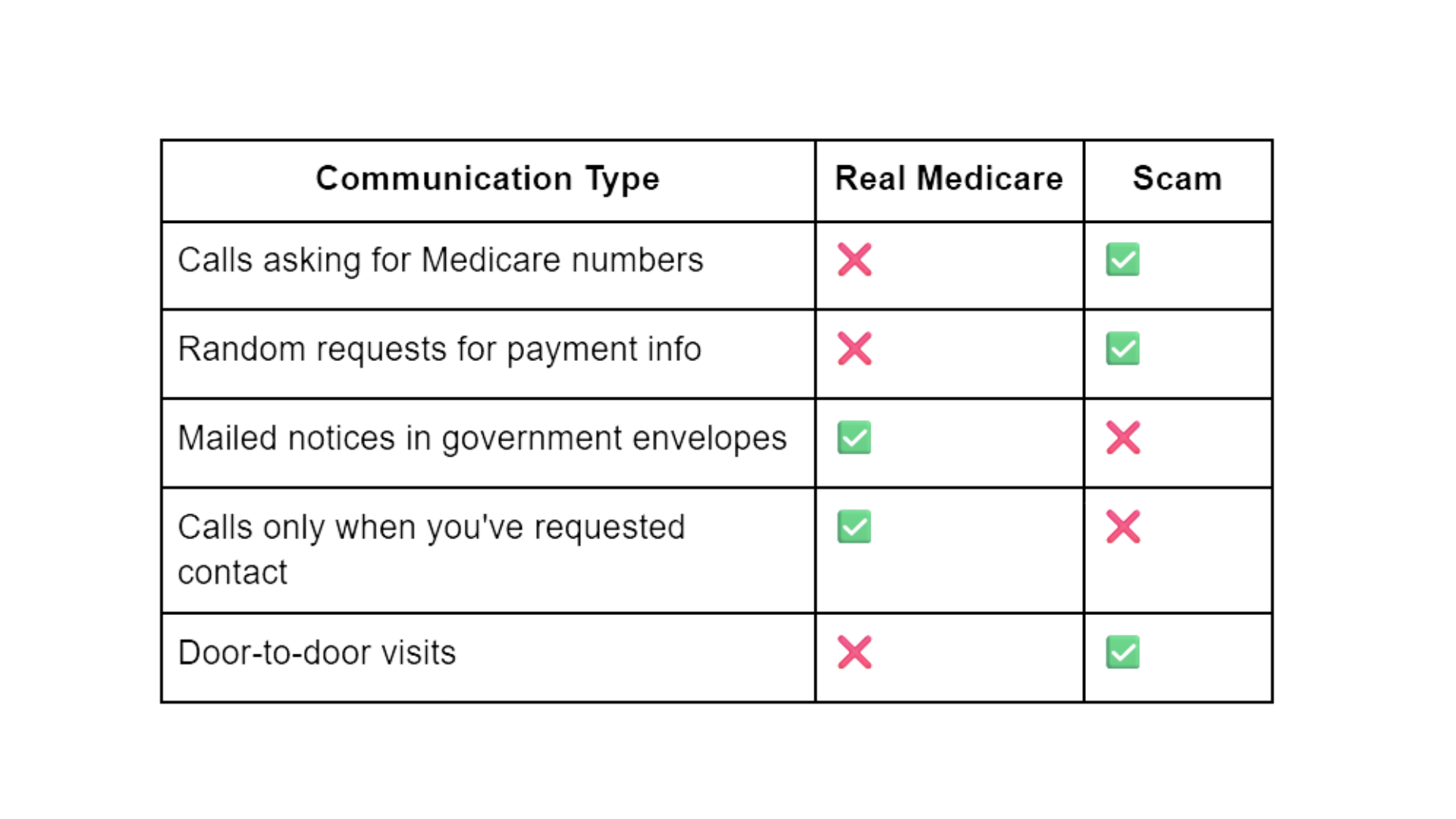

Navigating Medicare in 2025 is more complex than ever. From shifting plan rules to changing health needs, one small error can cost you thousands in penalties or lost benefits. Missing your enrollment window or underestimating Part D drug costs isn’t just frustrating—it can mean months without prescription coverage or a hefty late penalty. The stakes are high when premiums, copays, and deductibles keep climbing. This guide identifies the top 7 Medicare mistakes people commonly make and shows you exactly how to avoid them, with actionable, resource-backed solutions. Whether you're enrolling for the first time or reviewing your coverage, this post ensures you're fully informed—and armed.

🚨 AEP is Approaching – Act Now to Review or Update Your Medicare Coverage! The Annual Enrollment Period (AEP) begins October 15 —just weeks away. Whether you’re new to Medicare or considering a change in your plan, now is the critical time to prepare. Missing deadlines can result in higher costs, limited coverage, or no changes until next year. Use this guide to take control of your Medicare options before it’s too late.

Staying organized with your Medicare documents isn't just a matter of convenience—it’s essential for avoiding billing errors, ensuring timely coverage, and preparing for emergencies. In this guide, we provide comprehensive and actionable steps to help you maintain a secure, easy-to-access Medicare document management system. 1. Create a Centralized Medicare Document System Keeping all Medicare-related paperwork in one dedicated space is the cornerstone of effective organization. This includes: Medicare ID cards Annual Notice of Change (ANOC) Evidence of Coverage (EOC) Summary Notices (MSNs and EOBs) Prescription drug coverage details Correspondence from insurance carriers or CMS Bills and payment receipts Appeals and grievance letters Choose a method that suits your lifestyle: Physical filing system (binder or file cabinet with tabs) Digital storage (scanned PDFs organized in cloud folders) Pro Tip: Label your folders by category and year, e.g., EOBs_2025, Prescriptions_2024.

Navigating the Medicare enrollment process can seem overwhelming, but with the right guidance, signing up becomes a clear, manageable task. In this comprehensive guide, we’ll walk you through every step required to sign up for Medicare, including key dates, eligibility requirements, the different parts of Medicare, and how to avoid costly mistakes. Understanding Medicare Eligibility: Who Can Enroll? Most individuals become eligible for Medicare when they turn 65. However, eligibility can also be based on certain disabilities or medical conditions such as End-Stage Renal Disease (ESRD) or ALS (Lou Gehrig’s Disease). Key Medicare Eligibility Criteria: Age 65 or older U.S. citizen or legal permanent resident for at least 5 continuous years Under 65 with a qualifying disability (receiving Social Security Disability Insurance for 24 months) Diagnosed with ESRD or ALS Step 1: Know Your Medicare Enrollment Periods Enrolling at the right time is crucial to avoid penalties and coverage gaps. Medicare has specific enrollment windows you need to be aware of: Initial Enrollment Period (IEP) This is a 7-month window that includes: 3 months before your 65th birthday The month of your 65th birthday 3 months after your 65th birthday General Enrollment Period (GEP) January 1 to March 31 each year For those who missed their IEP Coverage starts July 1 Special Enrollment Period (SEP) If you're still working and covered under a group health plan, you may qualify for a SEP after your IEP ends. Annual Enrollment Period (AEP) October 15 to December 7 For making changes to existing Medicare Advantage or Part D plans Step 2: Understand the Parts of Medicare Before you enroll, it’s essential to understand how Medicare is structured. Each "Part" covers different services. Medicare Part A – Hospital Insurance Inpatient hospital stays Skilled nursing facility care Hospice care Some home health care Most people receive premium-free Part A if they or their spouse worked and paid Medicare taxes for at least 10 years. Medicare Part B – Medical Insurance Doctor visits Outpatient care Preventive services Durable medical equipment Standard premium for 2025 is $174.70/month (subject to income adjustments). Medicare Part C – Medicare Advantage Offered by private insurers Combines Part A and B (often includes Part D) May include extra benefits (e.g., vision, dental, hearing) Medicare Part D – Prescription Drug Coverage Covers prescription medications Standalone or bundled in a Medicare Advantage plan Step 3: Decide Between Original Medicare and Medicare Advantage You must choose between Original Medicare (Part A & B) with optional Part D and Medigap or a bundled Medicare Advantage Plan (Part C) . Feature: Doctors & Hospitals Prescription Coverage Additional Benefits Out-of-Pocket Maximum Original Medicare Any provider nationwide Not included (need Part D) None Varies (Part B + Medigap + D) No cap Medicare Advantage Network-based (HMO/PPO) Often included Vision, dental, hearing, etc. May have lower premiums Annual out-of-pocket max Step 4: Enroll in Medicare (How and Where) Enrolling in Medicare Part A and Part B If you're receiving Social Security benefits at 65, enrollment is automatic . Otherwise, apply in one of the following ways: Online a t SSA.gov/medicare By phone at 1-800-772-1213 In person at your local Social Security office Enrolling in Part C and Part D Compare plans at Medicare.gov Enroll through the plan’s website or by phone Work with a licensed insurance agent for personalized help Step 5: Consider Medigap (Medicare Supplement Insurance) Medigap fills in coverage gaps left by Original Medicare such as coinsurance, copayments, and deductibles. Key points: Must have Part A and B Can't be combined with Medicare Advantage Best time to buy: Medigap Open Enrollment Period (6 months starting the month you're 65 and enrolled in Part B) Step 6: Avoid Medicare Enrollment Penalties Failing to enroll in time can lead to lifelong penalties. Part B Late Enrollment Penalty 10% increase in premium for each full 12-month period you delay enrollment Part D Late Enrollment Penalty 1% of the national base premium times the number of full months you were late Final Thoughts Signing up for Medicare doesn’t have to be complicated. With a clear understanding of your eligibility, enrollment periods, and plan options, you can make confident decisions about your healthcare coverage. Whether you choose Original Medicare with Medigap and Part D or opt for a Medicare Advantage plan, proactive planning ensures you get the benefits you deserve without unnecessary penalties or gaps. For additional help, consult with a licensed Medicare advisor or visit Medicare.gov to explore plans available in your area.